》Check SMM minor metal quotes, data, and market analysis

》Subscribe to view historical spot prices of SMM titanium

Reviewing China's magnesium market in H1 2025, the long-term concentrated production halts at magnesium plants quietly reversed the supply-demand imbalance. Tight spot supply and low inventory levels created a solid foundation for periodic price increases in the magnesium ingot market. Market sentiment was frequently disrupted by news such as "solid waste burial," "dolomite mine shutdowns in the Wutai region," and "environmental protection checks deployment," leading to frequent price fluctuations.

Price Review

The magnesium ingot price trend in H1 2025 exhibited an overall pattern of low early levels followed by highs, jumping initially and then pulling back, with bottom-range fluctuations.

Phase 1: Procurement and Storage Provide Bottom Support, Prices Stabilize

Supply side, weakened demand left smelters in major production regions facing losses across the entire production cycle. Some announced formal production cuts, while winter conditions delayed resumptions at previously idled facilities, sustaining the downward trend in supply. Inventories at major producers reportedly fell to safe levels. Demand side, weak raw material prices fostered a wait-and-see sentiment among downstream enterprises, leading to cautious procurement.

Phase 2: Falling Raw Material Prices vs. Low Inventory, Prices Follow a "√" Trajectory

Pressured by sustained declines in raw material prices and tight cash flow at smelters, magnesium prices faced significant downward pressure. Smelters lowered prices to stimulate downstream demand, but this failed to alleviate liquidity issues and instead accelerated the plunge, with prices dropping nearly 1,000 yuan within half a month.

As prices hit 15,000 yuan/mt, foreign traders entered the market en masse, rapidly depleting circulating inventory and driving prices upward. Despite occasional pullbacks, the market remained in tight balance, with low inventory consistently supporting the floor. Prices eventually climbed to 17,400 yuan/mt.

Phase 3: Resumption Rumors Spread, Prices Peak and Retreat Amid Pessimism

With prices at elevated levels, buyers regained rationality, while small smelters offloaded stocks at lower prices, gradually shifting the price center downward. News of production resumptions further weighed on sentiment, as anticipated supply increases threatened to rebuild inventory pressure at smelters, reopening the downward channel. Prices retreated to 15,950 yuan/mt.

Production Review

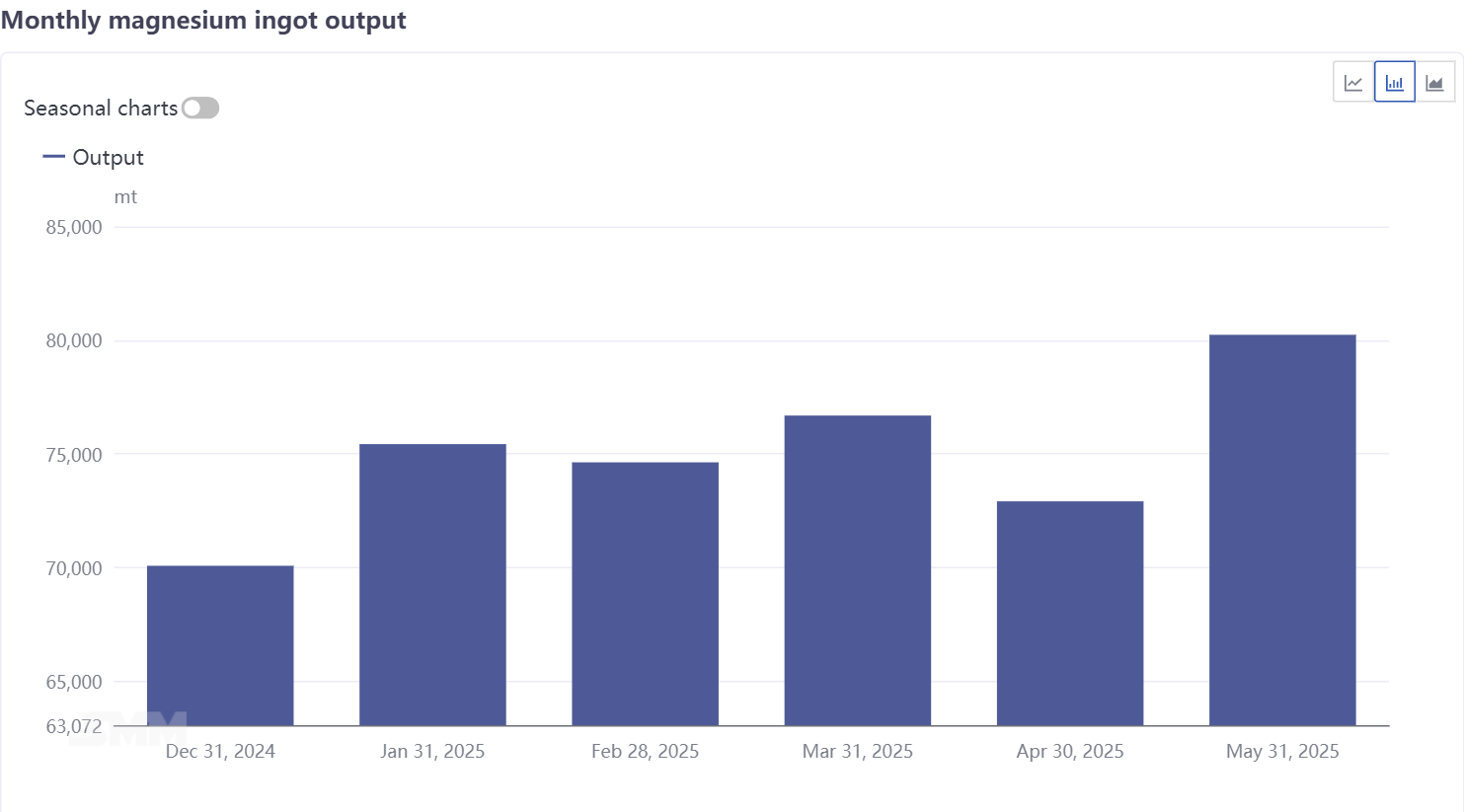

Primary magnesium output totaled 465,000 mt from January to June, up 3.0% MoM, while magnesium ingot production reached 414,000 mt, rising 2.6% MoM. Improved profitability due to rising prices enabled previously idled smelters to gradually resume output by late April to early May, slowly boosting production volumes.

Price Outlook

SMM analysis suggests that the current magnesium ingot market is facing a multi-faceted market scenario characterized by low inventory, low demand, and low costs. The low inventory levels provide a solid foundation for a phased increase in the magnesium ingot market fundamentals, with short-term explosive market demand capable of rapidly driving up market prices. However, the bearish sentiment among downstream customers, fueled by the negative signal of multiple magnesium plants resuming production, is strong. The current situation of low costs and low demand in the magnesium market results in weak support for magnesium prices. Overall, the resumption of production by multiple magnesium plants is likely to disrupt the existing tight balance between supply and demand, leading to a weak performance in magnesium prices. Considering the current magnesium market's significant reaction to centralized procurement, magnesium prices are expected to fluctuate frequently in the future, with a projected trend of fluctuating downward.

![[SMM Analysis] Futures Lack Momentum to Rise Further, Pre-Holiday Demand Stalls, and Stainless Steel Social Inventory Accumulation Intensifies](https://imgqn.smm.cn/usercenter/HBsPu20251217171723.jpeg)